Money and banking

| English | Chinese | Pinyin |

|---|---|---|

| barter | 物物交换 | wù wù jiāo huàn |

| medium of exchange | 交换媒介 | jiāo huàn méi jiè |

| unit of account | 记账单位 | jì zhàng dān wèi |

| store of value | 价值储藏 | jià zhí chǔ cáng |

| commercial banks | 商业银行 | shāng yè yín háng |

| central bank | 中央银行 | zhōng yāng yín háng |

| interest rate | 利率 | lì lǜ |

| lender of last resort | 最后贷款人 | zuì hòu dài kuǎn rén |

| money supply | 货币供给 | huò bì gōng jǐ |

What money actually does

- We take money for granted — but a working economy needs something everyone trusts to swap for goods. Strip money away and you're back to barter 物物交换.

- Money, and the banks that create and move it, are the plumbing of the whole economy.

Economics case lab

Classify real examples by the economic idea they show.

Match each function of money to its meaning.

The four classic functions of money.

The functions of money

Commercial banks 商业银行 take deposits and make loans, creating most of the money in the economy

Using money to compare the value of different goods is its role as a:

A unit of account lets us measure and compare values.

Commercial banks create money when they make loans.

Lending creates new deposits — most money is bank-created credit, not cash.

Which is a role of the central bank?

The central bank sets rates, regulates banks and acts as lender of last resort.

Banks and the central bank 中央银行

- Commercial banks take deposits and make loans — and in lending, they create money (credit).

- The central bank sets interest rates 利率, is the lender of last resort 最后贷款人, and regulates the banking system.

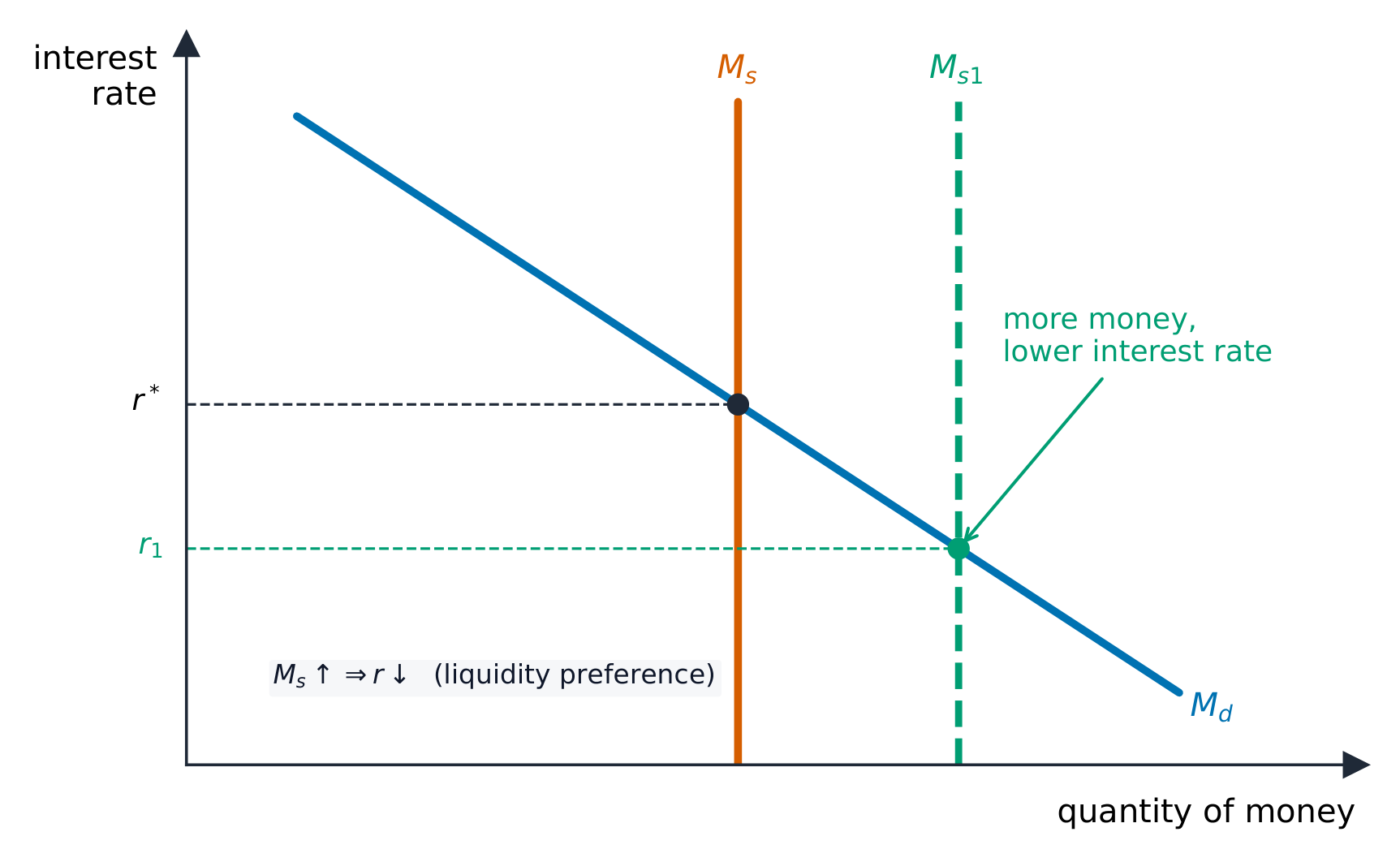

The interest rate set by the demand for and supply of money

The interest rate is the price of ______ money.

It is what borrowers pay (and savers receive).

Interest rates and the money supply 货币供给

- The interest rate is the price of borrowing money; the money supply is the total money in the economy.

- The central bank adjusts these to control inflation and support the economy (monetary policy).

Banks create most money. Most money isn't cash printed by the state — it's bank deposits created when commercial banks lend. That's why regulating lending matters.

You've got it

- money's four functions: medium of exchange, unit of account, store of value, standard of deferred payment

- commercial banks create money by lending; the central bank sets rates + is lender of last resort

- the interest rate is the price of borrowing; the money supply is total money