| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

PRD-1 | PRD-1.A |

|

Production, Cost, and the Perfect Competition Model

AP Microeconomics · Topic 3

3.1

The Production Function

Syllabus

Source: College Board AP Course and Exam Description

The production function 生产函数 links inputs to output. In the short run 短期 at least one input (usually capital) is fixed 固定; in the long run 长期 all inputs vary.

- Total product 总产量 is the total output.

- Marginal product 边际产量 (MP) is the extra output from one more unit of a variable input (usually labor): $MP=\dfrac{\Delta\ \text{output}}{\Delta\ \text{labor}}$.

- Average product 平均产量 is output per worker.

As you add workers to fixed capital, MP eventually falls – the law of diminishing marginal returns 边际收益递减法则. This shape of MP is what drives the shape of the cost curves below.

The production function turns inputs — labour and capital like this robot — into output

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| production function | 生产函数 | shēng chǎn hán shù |

| short run | 短期 | duǎn qī |

| fixed | 固定 | gù dìng |

| long run | 长期 | cháng qī |

| Total product | 总产量 | zǒng chǎn liàng |

| Marginal product | 边际产量 | biān jì chǎn liàng |

| Average product | 平均产量 | píng jūn chǎn liàng |

| law of diminishing marginal returns | 边际收益递减法则 | biān jì shōu yì dì jiǎn fǎ zé |

3.2

Short-Run Production Costs

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

PRD-1 | PRD-1.A |

|

Source: College Board AP Course and Exam Description

Costs split into fixed and variable:

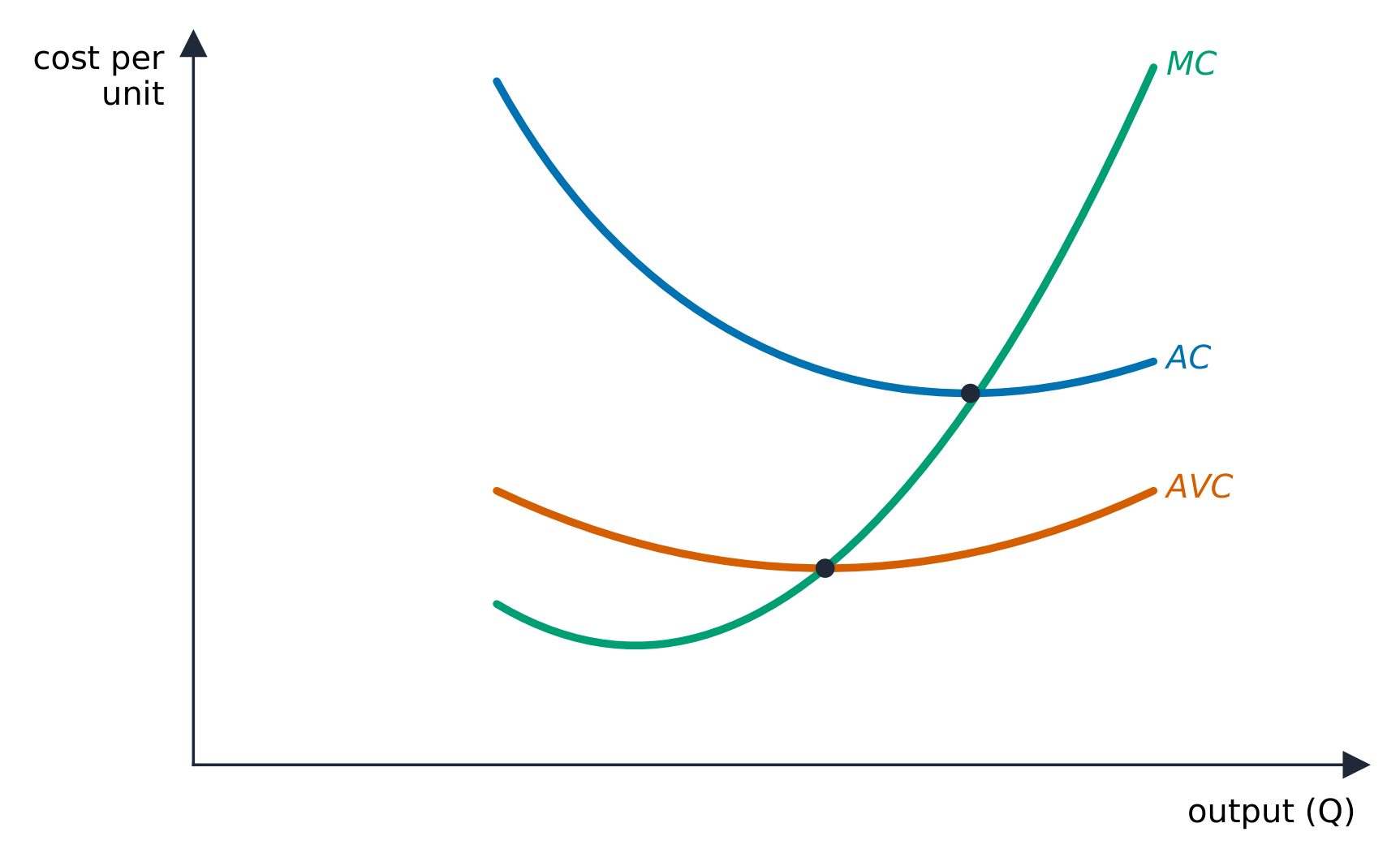

The short-run marginal, average, and average variable cost curves

- Fixed cost 固定成本 (FC) does not change with output (rent on the factory).

- Variable cost 可变成本 (VC) rises with output (materials, labor).

- Total cost 总成本 $TC=FC+VC$.

The per-unit costs matter most:

- Average fixed cost $AFC=FC/Q$ falls continuously (spreading fixed cost).

- Average variable cost $AVC=VC/Q$ and average total cost $ATC=TC/Q$ are U-shaped.

- Marginal cost 边际成本 $MC=\dfrac{\Delta TC}{\Delta Q}$ is the cost of one more unit.

Two key facts: MC is the mirror image of MP (when MP rises, MC falls, and vice versa), and MC cuts both AVC and ATC at their minimum points (when marginal is below average, the average falls; when above, it rises).

Worked example. A firm has fixed cost $FC=\$100$. At $Q=10$ its total cost is $\$300$, so variable cost is $\$200$: then $ATC=\tfrac{300}{10}=\$30$, $AVC=\tfrac{200}{10}=\$20$, and $AFC=\tfrac{100}{10}=\$10$ (note $AFC+AVC=ATC$). If raising output to $Q=11$ pushes total cost to $\$325$, the marginal cost of that $11$th unit is $\dfrac{\Delta TC}{\Delta Q}=\dfrac{325-300}{1}=\$25$.

Explore

Explore the U-shaped cost curves

As output rises, marginal cost eventually climbs (diminishing returns) and cuts through the U-shaped average cost at its minimum — the most efficient scale.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Fixed cost | 固定成本 | gù dìng chéng běn |

| Variable cost | 可变成本 | kě biàn chéng běn |

| Total cost | 总成本 | zǒng chéng běn |

| Marginal cost | 边际成本 | biān jì chéng běn |

3.3

Long-Run Production Costs

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

PRD-1 | PRD-1.A |

|

Source: College Board AP Course and Exam Description

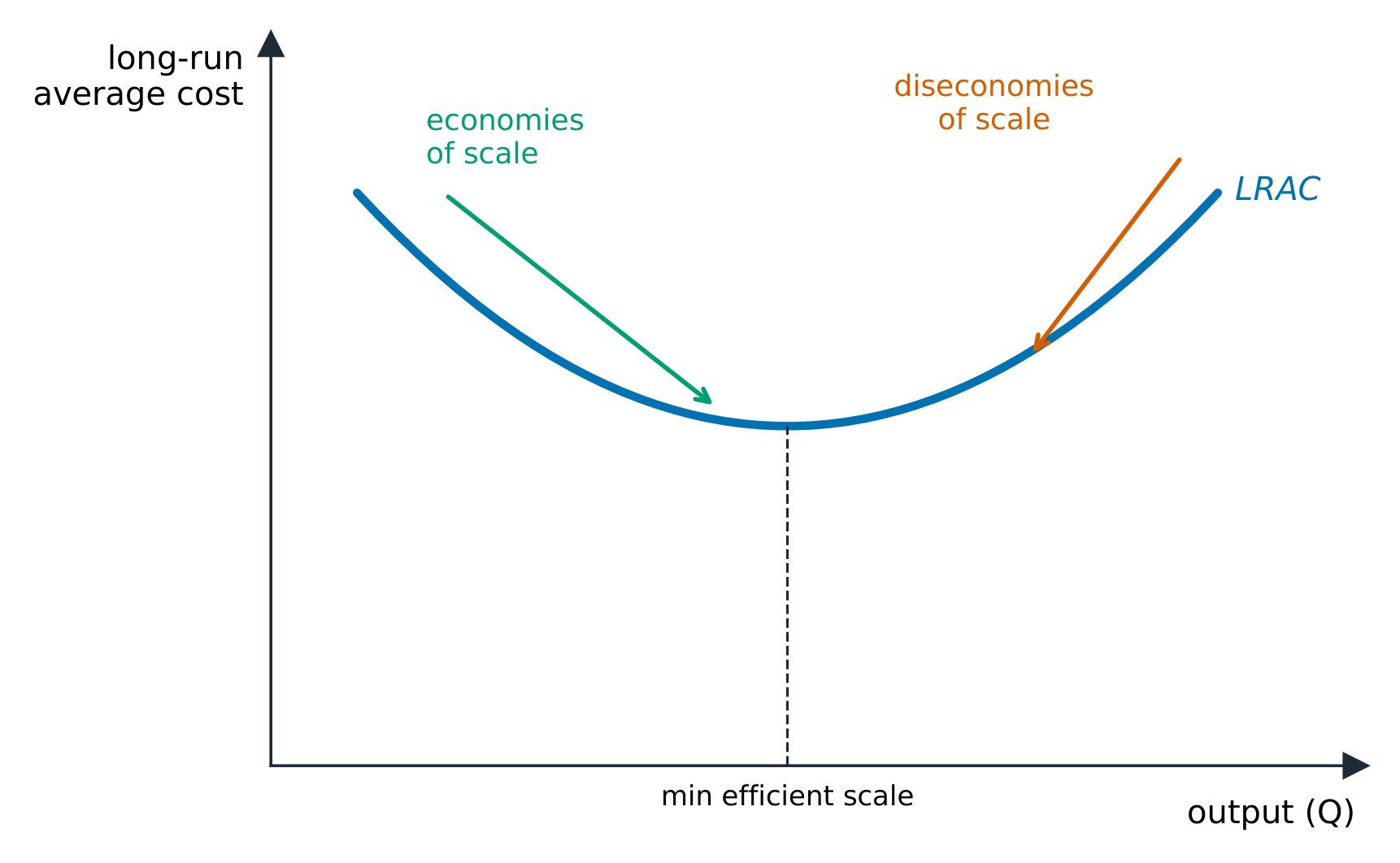

In the long run all inputs – including plant size – can change, so only the long-run average total cost (LRATC) curve matters. Its shape shows returns to scale:

Economies and diseconomies of scale on the long-run average cost curve

- Economies of scale 规模经济: LRATC falls as output grows (bulk buying, specialization).

- Constant returns to scale: LRATC flat.

- Diseconomies of scale 规模不经济: LRATC rises (a firm too big to manage well).

Exam skill: know that "diminishing returns" is a short-run idea (one fixed input) while "economies of scale" is a long-run idea (all inputs vary) – examiners test the distinction.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Economies of scale | 规模经济 | guī mó jīng jì |

| Diseconomies of scale | 规模不经济 | guī mó bù jīng jì |

3.4

Types of Profit

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

CBA-2 | CBA-2.C |

|

Source: College Board AP Course and Exam Description

Economists count all opportunity costs, including the owner's:

- Explicit costs 显性成本 are out-of-pocket payments; implicit costs 隐性成本 are the opportunity costs of owner-supplied resources (forgone salary, forgone interest).

- Accounting profit 会计利润 $=$ revenue $-$ explicit costs.

- Economic profit 经济利润 $=$ revenue $-$ explicit $-$ implicit costs.

Because economic profit subtracts more, it is smaller. Zero economic profit (a normal profit 正常利润) still means the owner is earning exactly the opportunity cost of their resources – a perfectly acceptable outcome.

Worked example. A shopkeeper takes in $\$200{,}000$ of revenue and pays $\$120{,}000$ in explicit costs, so accounting profit is $\$80{,}000$. But she gave up a $\$70{,}000$ salary elsewhere and $\$5{,}000$ of interest on the savings she invested – $\$75{,}000$ of implicit costs. Her economic profit is $80{,}000-75{,}000=\$5{,}000$: still positive, so staying in business genuinely beats her next-best alternative.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Explicit costs | 显性成本 | xiǎn xìng chéng běn |

| implicit costs | 隐性成本 | yǐn xìng chéng běn |

| Accounting profit | 会计利润 | kuài jì lì rùn |

| Economic profit | 经济利润 | jīng jì lì rùn |

| normal profit | 正常利润 | zhèng cháng lì rùn |

3.5

Profit Maximization

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

CBA-2 | CBA-2.D |

|

Source: College Board AP Course and Exam Description

Every firm, in every market structure, maximizes profit at the quantity where marginal revenue equals marginal cost:

$$MR=MC.$$

Produce each unit whose MR exceeds its MC; stop when they are equal. Producing less leaves profitable units unmade; producing more adds units that cost more than they earn.

3.6

Deciding to Produce, Enter, or Exit

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

PRD-2 | PRD-2.A |

|

Source: College Board AP Course and Exam Description

Even at $MR=MC$, a firm must check whether to operate:

- Short run – the shutdown rule: keep producing only if price covers average variable cost ($P\geq AVC$). If $P

- Profit check: compare $P$ to $ATC$ at the profit-maximizing quantity – $P>ATC$ means economic profit, $P

- Long run – entry and exit: economic profits attract entry 进入; losses cause exit 退出. This continues until economic profit is zero.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| entry | 进入 | jìn rù |

| exit | 退出 | tuì chū |

3.7

Perfect Competition

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

PRD-3 | PRD-3.A |

|

Source: College Board AP Course and Exam Description

A perfectly competitive 完全竞争 market has many small firms, an identical (homogeneous) product, free entry and exit, and perfect information. Each firm is a price taker 价格接受者 – too small to affect the price – so it faces a horizontal demand curve at the market price, and price = marginal revenue = average revenue ($P=MR=AR$).

This is why economists prize perfect competition. In long-run equilibrium it is both allocatively efficient 配置效率 and productively efficient 生产效率. Allocative efficiency holds because the firm produces where $P = MC$: the price (society's marginal benefit from the last unit) equals its marginal cost, so exactly the right amount is made. Productive efficiency holds because free entry drives price down to the minimum of average total cost, so goods are made as cheaply as possible. The market price is itself a signal that communicates everyone's marginal costs and benefits.

The market sets the price; the price-taking firm produces where MC = P, here with short-run profit

The side-by-side panel is the graph the exam wants: the market (left) fixes the price $P^{*}$; the firm (right) takes it as a horizontal line and produces where $MC=P$. When $P>ATC$ there is a short-run profit (the shaded box); that profit attracts entry, which shifts market supply right and pushes the price down.

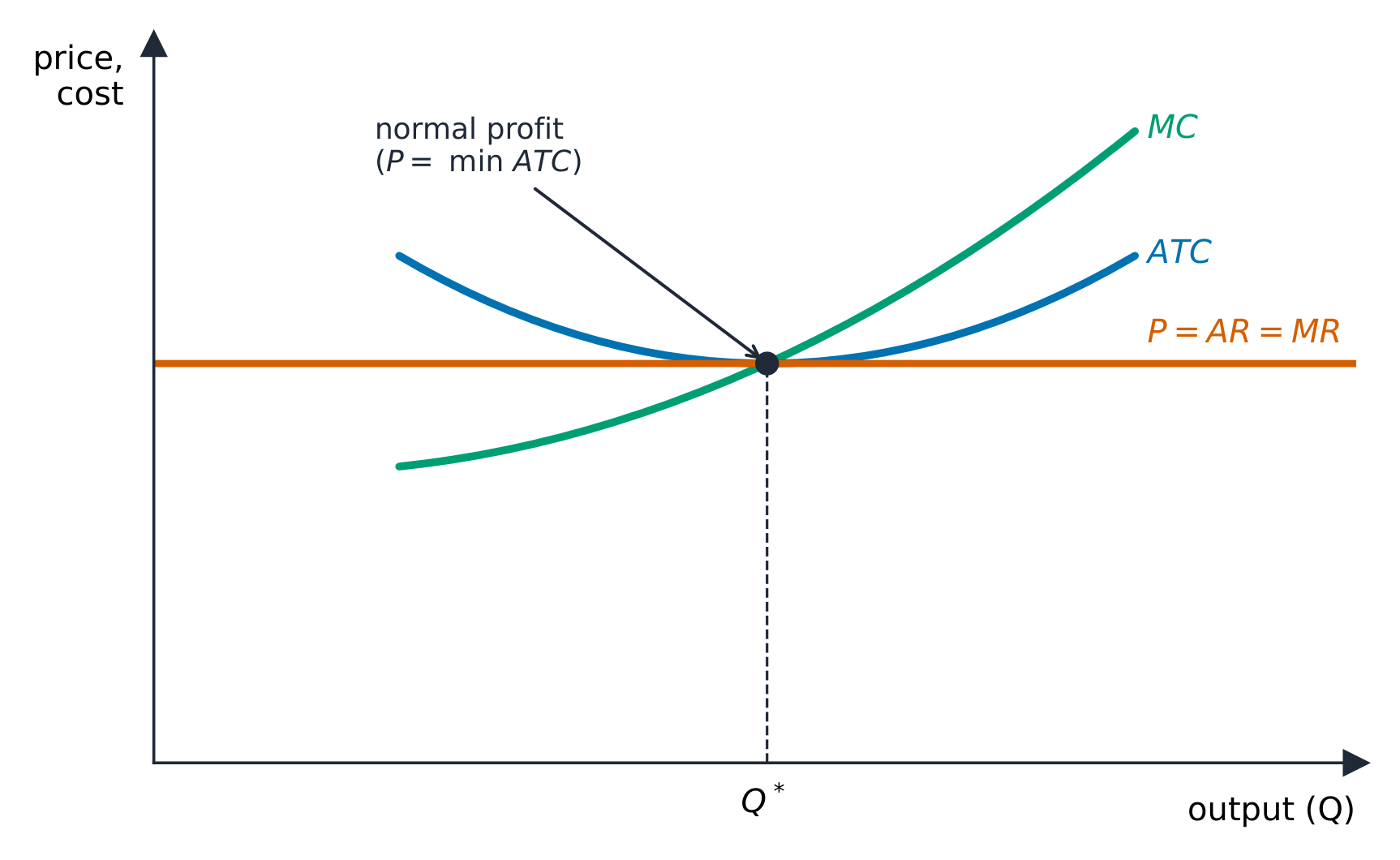

A perfectly competitive firm makes only normal profit in the long run

A perfectly competitive firm makes only normal profit in the long run

- Short run: the firm can earn profit, break even, or take a loss, producing where $P=MC$.

- Long run: entry and exit drive the firm to zero economic profit, producing where $P=MC=ATC$ at minimum ATC. This double efficiency – productive efficiency (lowest-cost output) and allocative efficiency ($P=MC$, so the last unit's value equals its cost) – is the benchmark against which every other market structure is judged.

Exam skill: be able to draw the side-by-side market and single-firm graphs, show a short-run profit or loss, then show how entry/exit restores long-run equilibrium at minimum ATC.

Explore

A price-taking firm in a competitive market

In perfect competition the market sets the price and each firm is a price-taker. It produces where price equals marginal cost, earning zero economic profit in the long run.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| perfectly competitive | 完全竞争 | wán quán jìng zhēng |

| price taker | 价格接受者 | jià gé jiē shòu zhě |

| allocatively efficient | 配置效率 | pèi zhì xiào lǜ |

| productively efficient | 生产效率 | shēng chǎn xiào lǜ |

3.7

Exam tips

- Know the cost curves: AFC falls, ATC/AVC are U-shaped, and MC cuts ATC and AVC at their minimums.

- Every firm maximises profit at MR = MC; check the shutdown rule ($P \ge AVC$ in the short run).

- Distinguish accounting profit (revenue − explicit costs) from economic profit (also minus implicit/opportunity costs); zero economic profit is normal.

- "Diminishing returns" is short-run (one fixed input); "economies of scale" is long-run (all inputs vary).

- In perfect competition $P=MR=AR$; entry/exit drive long-run economic profit to zero at minimum ATC.