| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

POL-1 | POL-1.F |

|

Long-Run Consequences of Stabilization Policies

AP Macroeconomics · Topic 5

5.1

Fiscal and Monetary Policy in the Short Run

Syllabus

Source: College Board AP Course and Exam Description

Both policies work by shifting AD in the short run. Fiscal policy 财政政策 changes government spending or taxes; monetary policy 货币政策 changes the money supply and thus the interest rate. They can work together (both expansionary to fight a deep recession) or be mixed (e.g. loose fiscal + tight monetary). In the short run, expansionary policy raises output and the price level and lowers unemployment; contractionary policy does the reverse.

Explore

Use policy to shift aggregate demand

In the short run, fiscal (spending/taxes) and monetary (interest-rate) policy shift aggregate demand, moving real GDP and the price level along short-run aggregate supply.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Fiscal policy | 财政政策 | cái zhèng zhèng cè |

| monetary policy | 货币政策 | huò bì zhèng cè |

5.2

The Phillips Curve

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

MOD-3 | MOD-3.A |

|

MOD-3.B |

|

Source: College Board AP Course and Exam Description

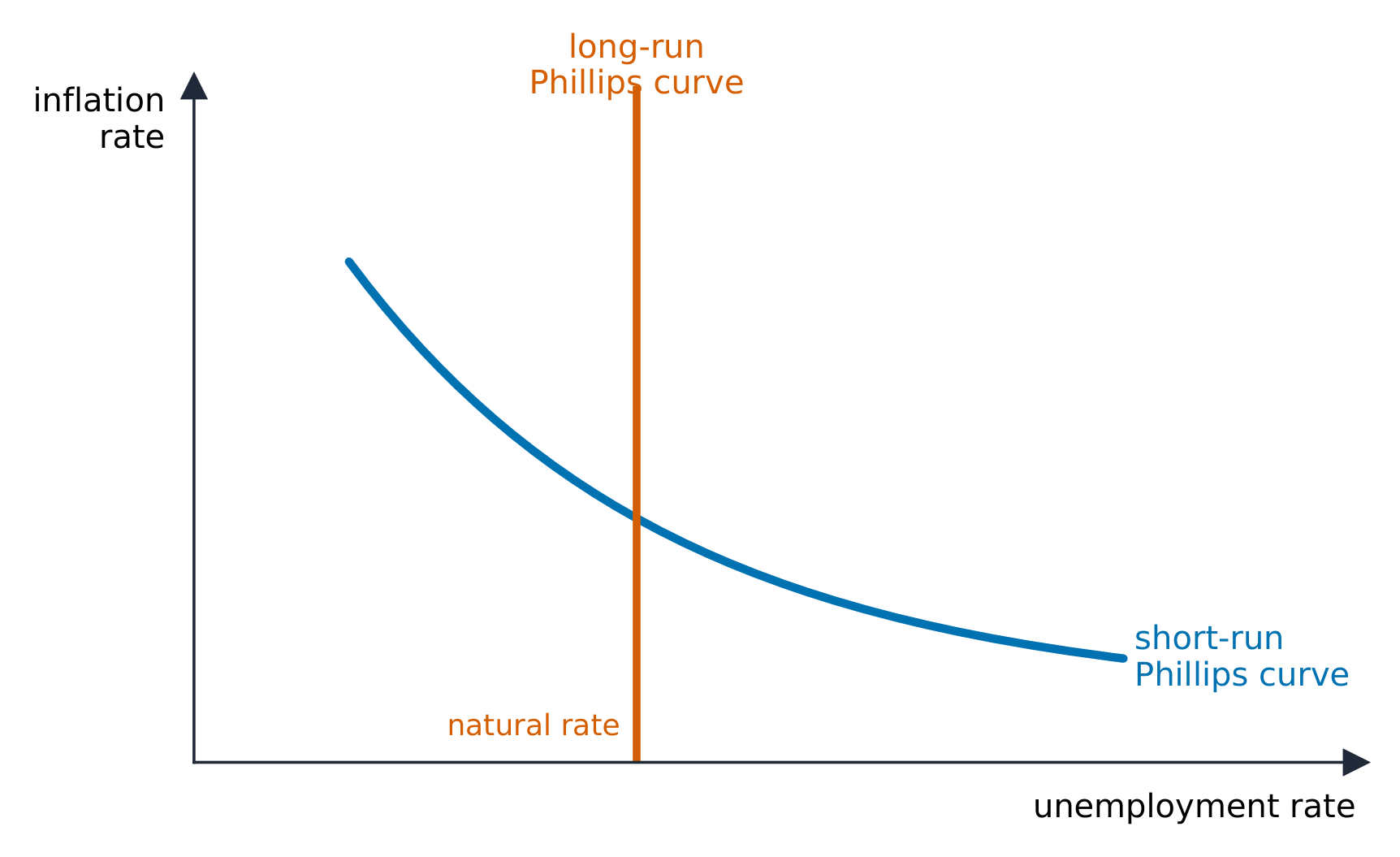

The Phillips curve 菲利普斯曲线 shows the short-run trade-off between inflation and unemployment:

The short-run and long-run Phillips curves

- The short-run Phillips curve (SRPC) 短期菲利普斯曲线 slopes downward – lower unemployment comes with higher inflation. It is the mirror image of AD-AS: a rightward AD shift moves the economy up-left along the SRPC (less unemployment, more inflation).

- The long-run Phillips curve (LRPC) 长期菲利普斯曲线 is vertical at the natural rate of unemployment 自然失业率 – the counterpart of vertical LRAS. In the long run there is no trade-off: policy changes inflation, not unemployment.

- A supply shock shifts the SRPC (a negative shock moves it right – worse inflation and unemployment, i.e. stagflation). A change in expected inflation also shifts the SRPC.

Exam skill: link the AD-AS and Phillips graphs – a recessionary gap in AD-AS corresponds to a point on the SRPC to the right of the natural rate; know what shifts SRPC versus moves along it.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Phillips curve | 菲利普斯曲线 | fēi lì pǔ sī qū xiàn |

| short-run Phillips curve (SRPC) | 短期菲利普斯曲线 | duǎn qī fēi lì pǔ sī qū xiàn |

| long-run Phillips curve (LRPC) | 长期菲利普斯曲线 | cháng qī fēi lì pǔ sī qū xiàn |

| natural rate of unemployment | 自然失业率 | zì rán shī yè lǜ |

5.3

Money Growth and Inflation

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

POL-3 | POL-3.A |

|

Source: College Board AP Course and Exam Description

In the long run, inflation is a monetary phenomenon. The quantity theory of money 货币数量论 states $M\times V = P\times Y$ (money supply $\times$ velocity $=$ price level $\times$ real output). With velocity $V$ and real output $Y$ roughly stable in the long run, growth in the money supply translates almost one-for-one into inflation. Printing money faster than the economy grows raises the price level, not real output – the root of high inflation and, in the extreme, hyperinflation 恶性通货膨胀.

Worked example. Suppose the money supply grows $8\%$ per year while real output $Y$ grows $3\%$ and velocity $V$ is stable. Rearranging $M\times V=P\times Y$ into growth rates, inflation $\approx 8\%-3\%=5\%$. The $5\%$ of money growth not matched by extra output simply becomes higher prices.

Explore

Link money growth to inflation

The quantity theory $MV=PY$: with output and velocity roughly fixed, the price level moves in proportion to the money supply — too much money chasing the same goods is inflation.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| quantity theory of money | 货币数量论 | huò bì shù liàng lùn |

| hyperinflation | 恶性通货膨胀 | è xìng tōng huò péng zhàng |

5.4

Government Deficits and the National Debt

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

POL-3 | POL-3.B |

|

Source: College Board AP Course and Exam Description

A budget deficit 预算赤字 occurs when government spending exceeds tax revenue in a year (a surplus 盈余 is the reverse). The accumulated total of past deficits is the national debt 国债. Deficits are financed by borrowing – selling government bonds – which adds to the debt and to future interest payments. Persistent deficits raise concerns about crowding out and the burden of servicing the debt.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| budget deficit | 预算赤字 | yù suàn chì zì |

| surplus | 盈余 | yíng yú |

| national debt | 国债 | guó zhài |

5.5

Crowding Out

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

POL-3 | POL-3.C |

|

Source: College Board AP Course and Exam Description

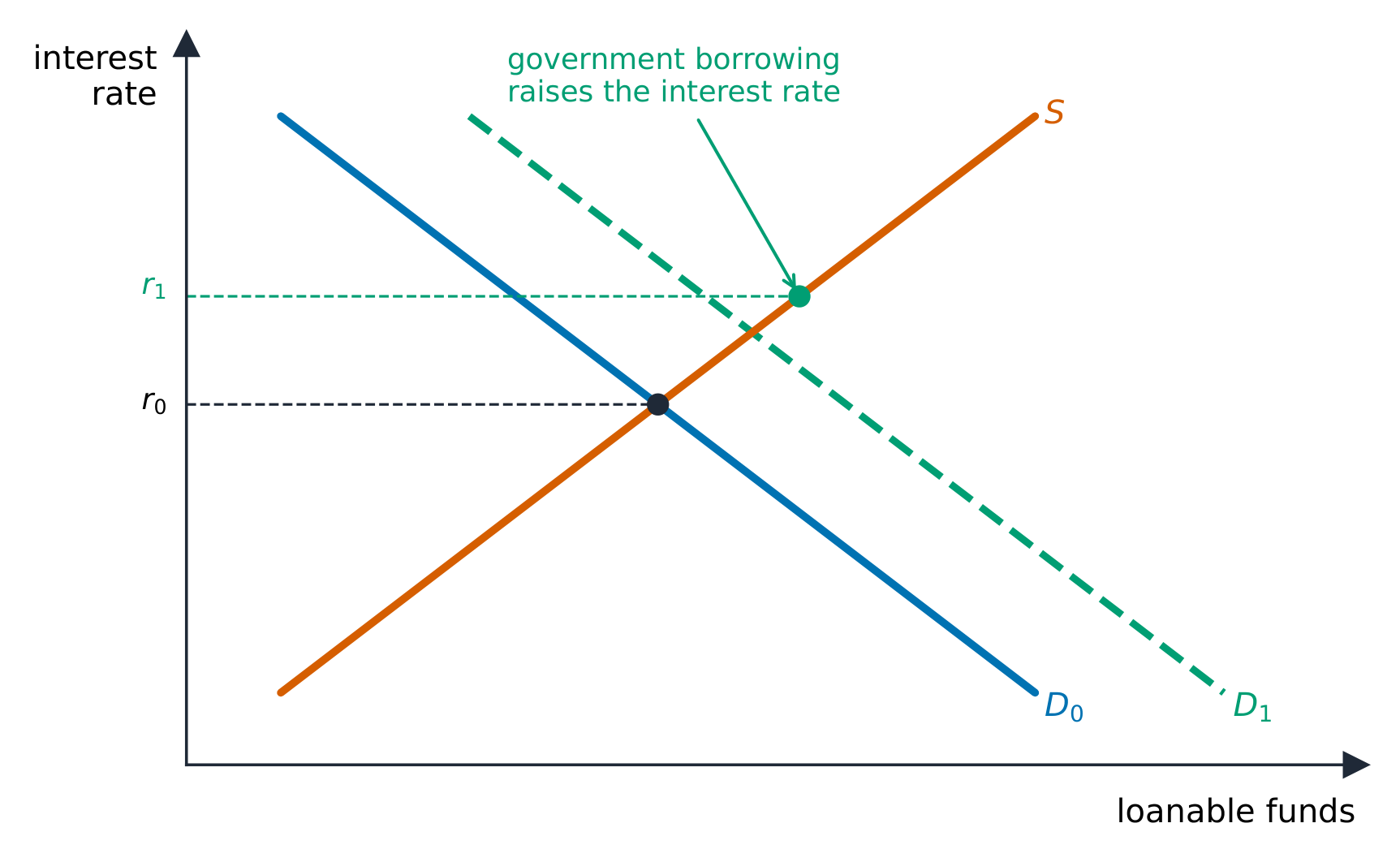

Crowding out 挤出效应 is the main long-run cost of deficit-financed fiscal policy. When the government borrows heavily, it increases the demand for loanable funds, raising the real interest rate. Higher rates reduce private investment (and interest-sensitive consumption). So expansionary fiscal policy partly cancels itself: the AD boost is offset by weaker investment. Worse, less investment today means a smaller capital stock and slower long-run growth.

Government borrowing raises interest rates and crowds out private investment

Exam skill: show crowding out on the loanable funds graph – government borrowing shifts demand right, the real interest rate rises, and private investment falls.

Worked example. A government borrows $\$500$ billion to finance a deficit. On the loanable funds market this shifts the demand for funds right, pushing the real interest rate up (say from $3\%$ to $4\%$). At the higher rate firms scale back investment – perhaps by $\$150$ billion – so the net boost to AD is smaller than the $\$500$ billion, and the lost investment slows long-run growth.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Crowding out | 挤出效应 | jǐ chū xiào yìng |

5.6

Economic Growth

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

MEA-2 | MEA-2.B |

|

Source: College Board AP Course and Exam Description

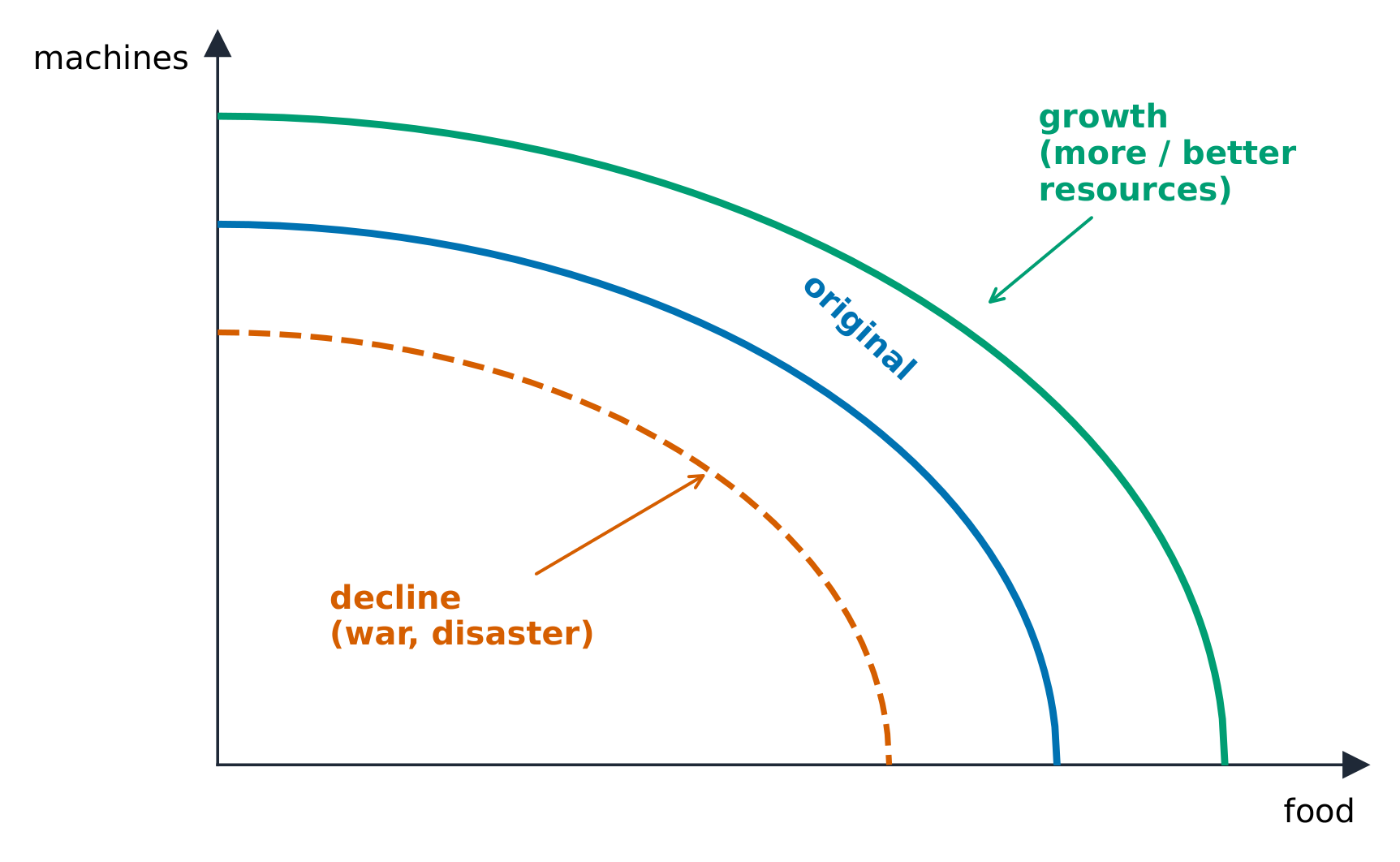

Economic growth 经济增长 is a sustained rise in real GDP per capita – the true source of higher living standards. It comes from more or better resources and is shown as a rightward shift of LRAS (and an outward shift of the PPC). Its main drivers:

Economic growth shifts the production possibilities curve outward

- physical capital 实物资本 (more tools and machines per worker),

- human capital 人力资本 (education, skills, health),

- technology 技术 and innovation,

- productivity 生产率 (output per worker) growth, the deepest driver.

Explore

Economic growth pushes the frontier out

Economic growth — more resources, better technology — shifts the whole production possibilities frontier outward, letting the economy produce more of everything.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Economic growth | 经济增长 | jīng jì zēng zhǎng |

| physical capital | 实物资本 | shí wù zī běn |

| human capital | 人力资本 | rén lì zī běn |

| technology | 技术 | jì shù |

| productivity | 生产率 | shēng chǎn lǜ |

5.7

Public Policy and Economic Growth

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

POL-4 | POL-4.A |

|

Source: College Board AP Course and Exam Description

Governments can raise long-run growth by policies that build capital and productivity: investment in infrastructure and education, research and development incentives, protecting property rights 产权 and the rule of law, encouraging saving and investment (which finances capital), and keeping inflation low and stable. The recurring long-run theme: policies that crowd out or discourage investment slow growth, while those that encourage capital formation speed it up.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| property rights | 产权 | chǎn quán |

5.7

Exam tips

- The short-run Phillips curve shows the inflation–unemployment trade-off; the long-run curve is vertical at the natural rate.

- In the long run inflation is a monetary phenomenon (money growth beyond output growth → inflation).

- Show crowding out on the loanable-funds graph: government borrowing raises the real rate and cuts private investment.

- Growth comes from more/better resources — physical capital, human capital, technology — shifting LRAS right.

- A supply shock moves inflation and unemployment the same way (stagflation), unlike a demand shock.