| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

MEA-3 | MEA-3.A |

|

Financial Sector

AP Macroeconomics · Topic 4

4.1

Financial Assets

Syllabus

Source: College Board AP Course and Exam Description

A financial asset 金融资产 is a claim that stores value: money, stocks 股票 (ownership shares), bonds 债券 (loans that pay interest), and bank deposits. Assets trade off liquidity 流动性 (how easily converted to cash), risk, and return. A key inverse relationship: bond prices and interest rates move in opposite directions – when market interest rates rise, existing bonds paying the old, lower rate are worth less, so their price falls.

A stock exchange is where financial assets are bought and sold, setting prices from supply and demand

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| financial asset | 金融资产 | jīn róng zī chǎn |

| stocks | 股票 | gǔ piào |

| bonds | 债券 | zhài quàn |

| liquidity | 流动性 | liú dòng xìng |

4.2

Nominal versus Real Interest Rates

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

MEA-3 | MEA-3.B |

|

Source: College Board AP Course and Exam Description

- The nominal interest rate 名义利率 is the stated rate, not adjusted for inflation.

- The real interest rate 实际利率 is what you actually earn in purchasing power:

$$\text{real rate}\approx\text{nominal rate}-\text{inflation rate}\quad(\text{Fisher equation}).$$

Lenders and borrowers care about the real rate. If inflation turns out higher than expected, real rates fall – helping borrowers and hurting lenders.

Worked example. A loan carries a nominal rate of $6\%$ while inflation runs at $2\%$. The real rate is $6\%-2\%=4\%$, so the lender's purchasing power grows by $4\%$. If inflation instead jumped to $7\%$, the real rate would be $-1\%$ – the lender would actually lose purchasing power.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| nominal interest rate | 名义利率 | míng yì lì lǜ |

| real interest rate | 实际利率 | shí jì lì lǜ |

4.3

The Definition, Measurement, and Functions of Money

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

MEA-3 | MEA-3.C |

|

Source: College Board AP Course and Exam Description

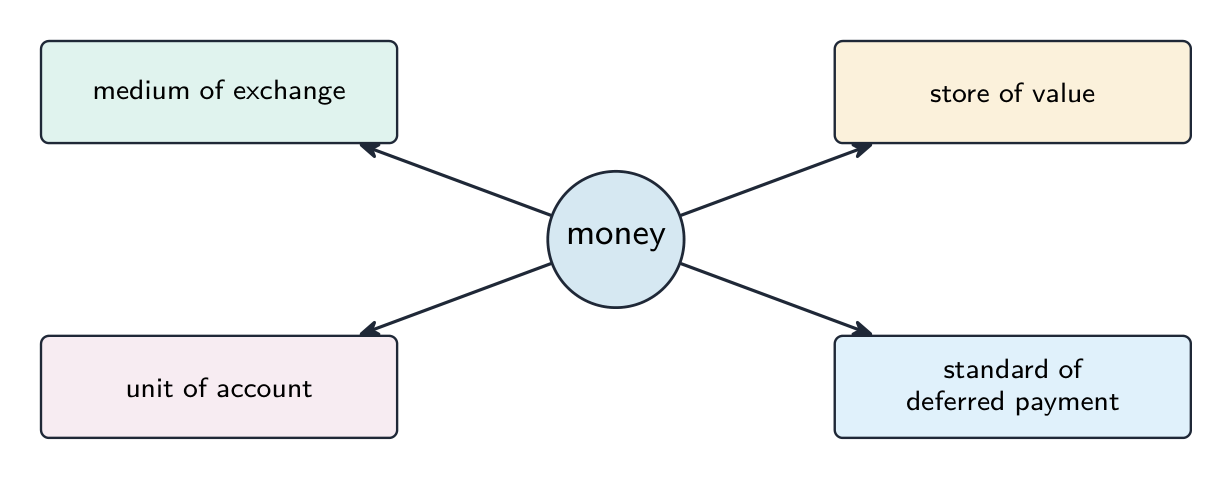

Money 货币 is anything widely accepted in exchange. Its three functions: a medium of exchange 交换媒介 (avoids barter), a unit of account 记账单位 (a common measure of value), and a store of value 价值储藏 (holds value over time). Modern money is fiat money 法定货币 – valuable because the government declares it legal tender and people trust it, not because it is backed by gold.

The four functions of money

Money is measured in tiers by liquidity: M1 (currency plus checkable deposits – the most liquid) and the broader M2 (M1 plus savings deposits and other near-money). Below M1 is the monetary base 基础货币 (M0, or MB) – currency in circulation plus bank reserves. The money multiplier equals money supply ÷ monetary base, so a central-bank action that raises reserves expands the money supply by a larger amount through the multiplier.

Money works because everyone accepts it: a shared unit of account, medium of exchange, and store of value

Money works because everyone accepts it: a shared unit of account, medium of exchange, and store of value

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Money | 货币 | huò bì |

| medium of exchange | 交换媒介 | jiāo huàn méi jiè |

| unit of account | 记账单位 | jì zhàng dān wèi |

| store of value | 价值储藏 | jià zhí chǔ cáng |

| fiat money | 法定货币 | fǎ dìng huò bì |

| monetary base | 基础货币 | jī chǔ huò bì |

4.4

Banking and the Expansion of the Money Supply

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

POL-2 | POL-2.A |

|

Source: College Board AP Course and Exam Description

Banks operate on a fractional reserve 部分准备金 system: they keep a fraction of deposits as reserves 准备金 and lend the rest. The fraction they must keep is the required reserve ratio 法定准备金率 (rr). Lending creates new deposits, which are re-deposited and re-lent, expanding the money supply by the money multiplier:

$$\text{money multiplier}=\frac{1}{rr}.$$

A new $1000 deposit with$rr=0.1$can expand the money supply by up to$1000\times\frac{1}{0.1}=10,000$. Use a bank's T-account (assets = reserves + loans; liabilities = deposits) to track required reserves and excess reserves 超额准备金 (the amount available to lend).

Worked example. A bank receives a $\$1000$ deposit with $rr=0.20$. It must hold $0.20\times1000=\$200$ as required reserves, leaving $\$800$ of excess reserves to lend. With a money multiplier of $\dfrac{1}{0.20}=5$, that $\$800$ of new lending can expand the money supply by up to $800\times5=\$4000$ across the banking system.

Exam skill: given a required reserve ratio and a deposit, compute excess reserves, the money multiplier, and the maximum change in the money supply.

Explore

See banks multiply deposits

Banks keep a fraction of deposits as reserves and lend the rest, which is redeposited and lent again — the money multiplier expands the money supply from the initial deposit.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| fractional reserve | 部分准备金 | bù fèn zhǔn bèi jīn |

| reserves | 准备金 | zhǔn bèi jīn |

| required reserve ratio | 法定准备金率 | fǎ dìng zhǔn bèi jīn lǜ |

| excess reserves | 超额准备金 | chāo é zhǔn bèi jīn |

4.5

The Money Market

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

MKT-3 | MKT-3.A |

|

MKT-3.B |

| |

MKT-3.C |

| |

MKT-3.D |

|

Source: College Board AP Course and Exam Description

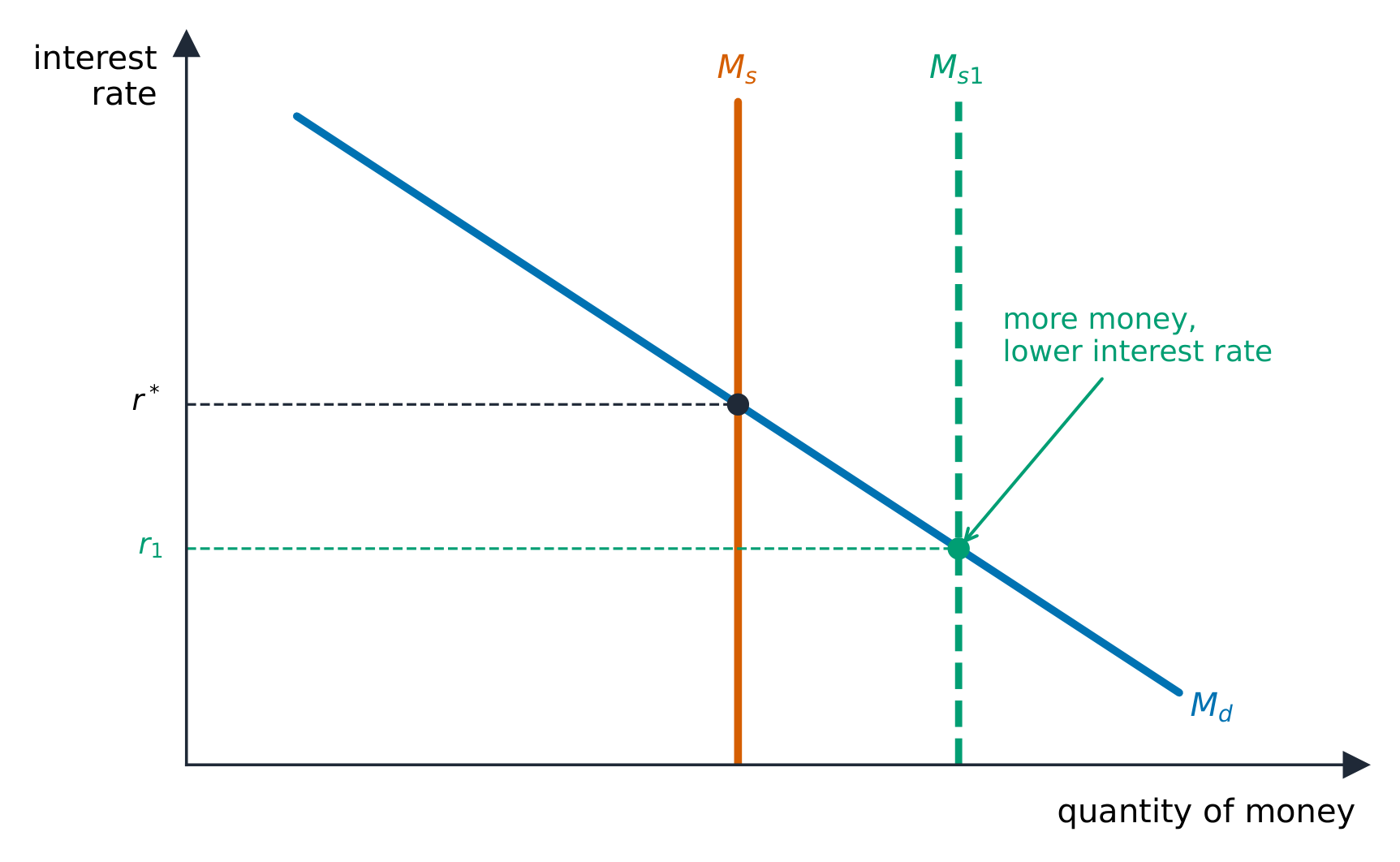

The money market 货币市场 determines the nominal interest rate:

The interest rate is set by the demand for and supply of money

- Money demand 货币需求 slopes downward against the interest rate – the rate is the opportunity cost of holding money instead of interest-bearing assets. It shifts right with a higher price level or more real GDP.

- Money supply 货币供给 is vertical – set by the central bank, independent of the interest rate.

Their intersection sets the equilibrium interest rate. If the central bank increases the money supply, the supply line shifts right and the interest rate falls.

Explore

Equilibrium in the money market

The money market sets the interest rate where money demand meets the central bank's money supply. A change in the money supply moves the interest rate.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| money market | 货币市场 | huò bì shì chǎng |

| Money demand | 货币需求 | huò bì xū qiú |

| Money supply | 货币供给 | huò bì gōng jǐ |

4.6

Monetary Policy

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

POL-1 | POL-1.D |

|

POL-1.E |

|

Source: College Board AP Course and Exam Description

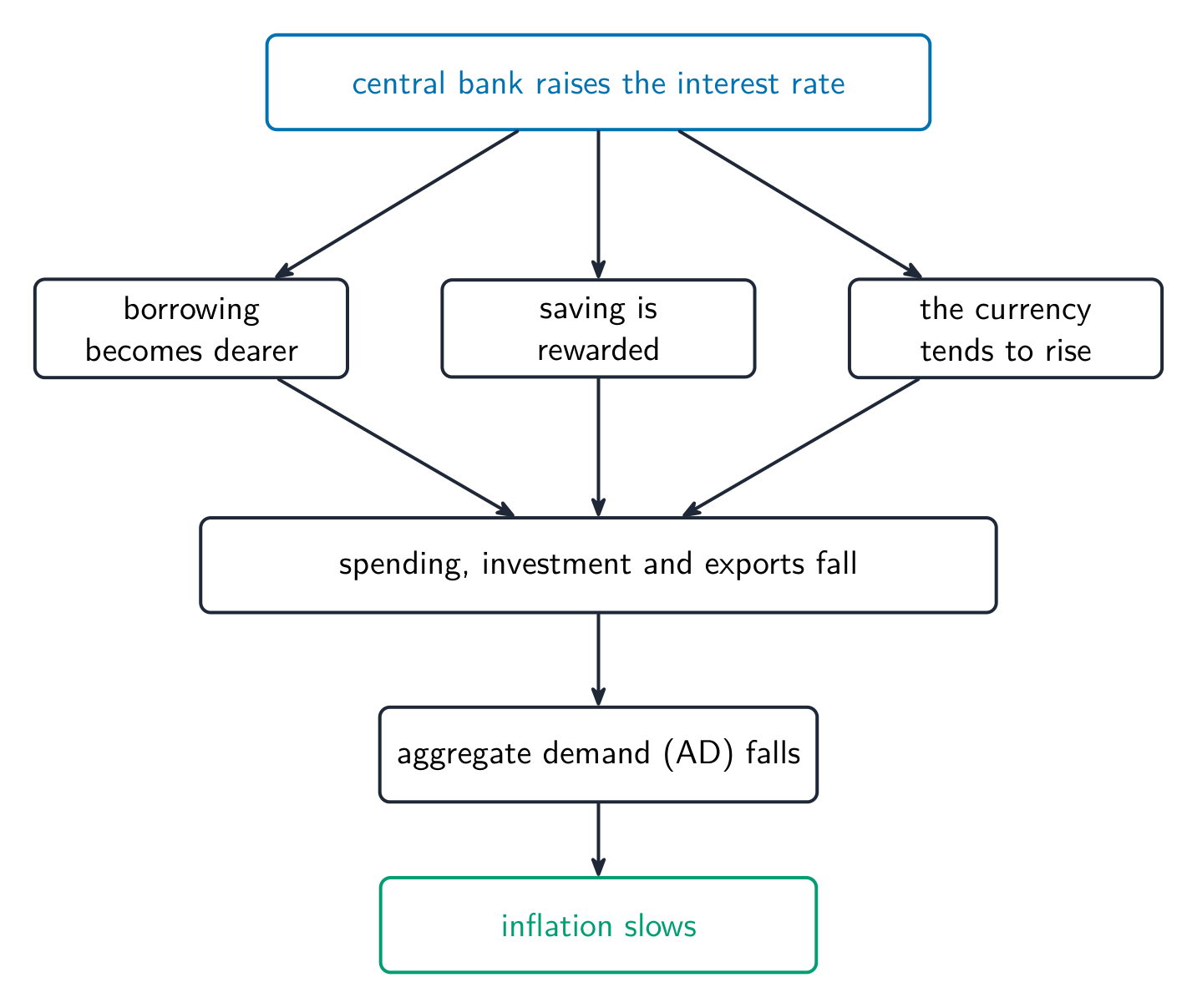

Monetary policy 货币政策 is the central bank's (the Federal Reserve's) use of the money supply to steer the economy, working through the interest rate:

How a higher interest rate works through the economy to slow inflation

- Expansionary (easy) 扩张性: increase the money supply $\to$ interest rate falls $\to$ investment and consumption rise $\to$ AD shifts right (fights recession).

- Contractionary (tight) 紧缩性: decrease the money supply $\to$ interest rate rises $\to$ AD shifts left (fights inflation).

Tools: open-market operations 公开市场操作 (buying bonds injects money, selling bonds withdraws it – the main tool), changing the reserve requirement, and changing the discount rate 贴现率 (the rate banks pay to borrow from the central bank). Follow the full chain on the exam: money supply $\to$ interest rate $\to$ investment $\to$ AD $\to$ output, price level, unemployment.

Modern central banks run an ample-reserves system. Rather than nudging the money supply, the Fed sets administered rates – chiefly the interest on reserves (IOR) 准备金利息 it pays banks – and this steers the policy rate 政策利率 (the federal funds rate, the overnight rate banks charge one another). In the reserve market, reserve demand slopes downward while the central bank supplies reserves at its chosen rate; raising IOR lifts the whole policy rate to fight inflation, lowering it eases to fight recession. (In the older limited-reserves system the Fed instead shifted the reserve supply through open-market operations.)

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| Monetary policy | 货币政策 | huò bì zhèng cè |

| Expansionary (easy) | 扩张性 | kuò zhāng xìng |

| Contractionary (tight) | 紧缩性 | jǐn suō xìng |

| open-market operations | 公开市场操作 | gōng kāi shì chǎng cāo zuò |

| discount rate | 贴现率 | tiē xiàn lǜ |

| interest on reserves (IOR) | 准备金利息 | zhǔn bèi jīn lì xī |

| policy rate | 政策利率 | zhèng cè lì lǜ |

4.7

The Loanable Funds Market

Syllabus

| Enduring Understanding | Learning Objective | Essential Knowledge |

|---|---|---|

MKT-4 | MKT-4.A |

|

MKT-4.B |

| |

MKT-4.C |

| |

MKT-4.D |

| |

MKT-4.E |

|

Source: College Board AP Course and Exam Description

The loanable funds market 可贷资金市场 determines the real interest rate and connects saving to investment:

- Supply of loanable funds comes from saving and slopes upward.

- Demand for loanable funds comes from borrowers (firms investing, government borrowing) and slopes downward.

That saving is the economy's national savings 国民储蓄 = private savings (households and firms) + public savings (the government's budget balance – a surplus adds to saving, a deficit subtracts from it). For an open economy, investment = national savings + net capital inflow from abroad. So a bigger budget deficit is negative public saving that shrinks the supply of loanable funds and crowds out investment.

More saving shifts supply right and lowers the real rate; more government borrowing shifts demand right and raises the real rate – the mechanism behind crowding out. Distinguish the two graphs: the money market sets the nominal rate (vertical money supply), while loanable funds sets the real rate (upward-sloping saving supply).

Exam skill: know which graph to draw – money market for monetary policy, loanable funds for saving, deficits, and crowding out – and trace how a shift in one feeds into AD-AS.

Vocabulary

Train

| English | Chinese | Pinyin |

|---|---|---|

| loanable funds market | 可贷资金市场 | kě dài zī jīn shì chǎng |

| national savings | 国民储蓄 | guó mín chǔ xù |

4.7

Exam tips

- Know money's three functions and the M1/M2 measures.

- The money market sets the nominal interest rate (vertical money supply); more money supply lowers the rate.

- Compute the money multiplier $\tfrac{1}{rr}$ and the maximum change in the money supply from a new deposit.

- Trace monetary policy: money supply → interest rate → investment → AD → output.

- Distinguish the money market (nominal rate) from the loanable-funds market (real rate); use the real rate $=$ nominal $-$ inflation.