Income statements

| English | Chinese | Pinyin |

|---|---|---|

| income statement | 损益表 | sǔn yì biǎo |

| revenue | 收入 | shōu rù |

| cost of sales | 销售成本 | xiāo shòu chéng běn |

| gross profit | 毛利润 | máo lì rùn |

| expenses | 费用 | fèi yòng |

| lenders | 放贷方 | fàng dài fāng |

Did it make a profit?

- At the end of the year, every business asks: did we make a profit?

- The income statement 损益表 answers it, by setting revenue 收入 against costs.

Financial statements flow

See how business events become the statements users read.

Revenue is 200 and cost of sales is 130. What is the gross profit?

Gross profit = 200 − 130 = 70.

Gross profit is 70 and expenses are 45. What is the profit?

Profit = 70 − 45 = 25.

Revenue minus cost of sales gives ______ profit.

Gross profit, before expenses are deducted.

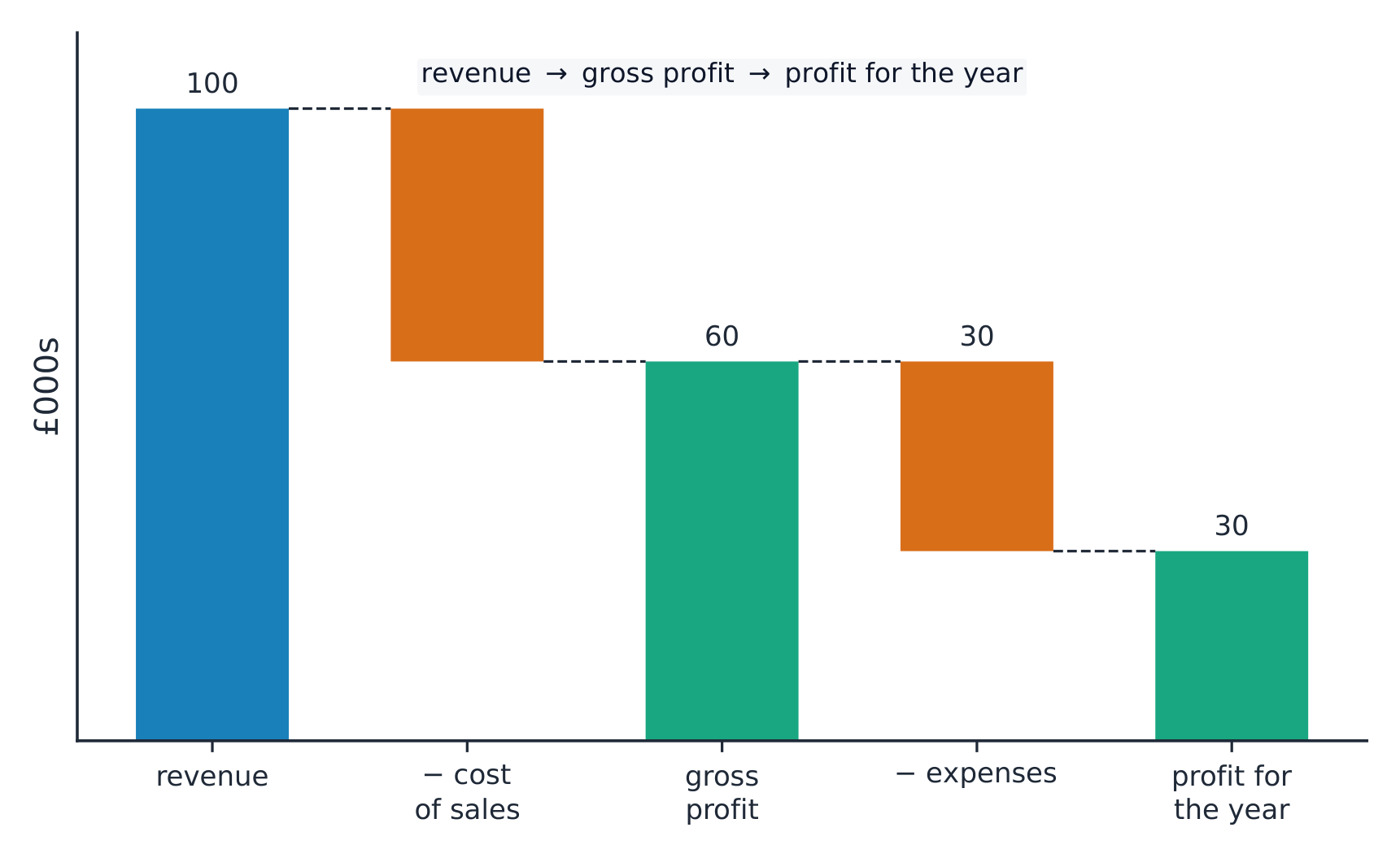

From revenue to profit

- Revenue is the money from sales.

- Revenue − cost of sales 销售成本 = gross profit 毛利润.

- Gross profit − expenses 费用 = profit (for the period).

Worked example. Revenue 150, cost of sales 90 → gross profit = 60. Expenses 35 → profit = 60 − 35 = 25.

An income statement falls from revenue to the profit for the year

Cost of sales is:

Cost of sales is the direct cost of producing the goods sold.

Cost of sales and expenses

- Cost of sales: the direct cost of the goods sold (materials, making them).

- Expenses: other running costs (rent, salaries, marketing).

Gross profit is the final profit after all costs are deducted.

Expenses must still be taken off gross profit to get the real profit.

Who uses it

- Owners check the profit; lenders 放贷方 judge whether they'll be repaid; managers plan ahead.

Gross profit is not the final profit. Gross profit only takes off the cost of sales. The expenses (rent, wages, etc.) must still be deducted to get the real profit.

You've got it

- revenue − cost of sales = gross profit

- gross profit − expenses = profit for the period

- the income statement shows whether the business made a profit, and is read by many stakeholders